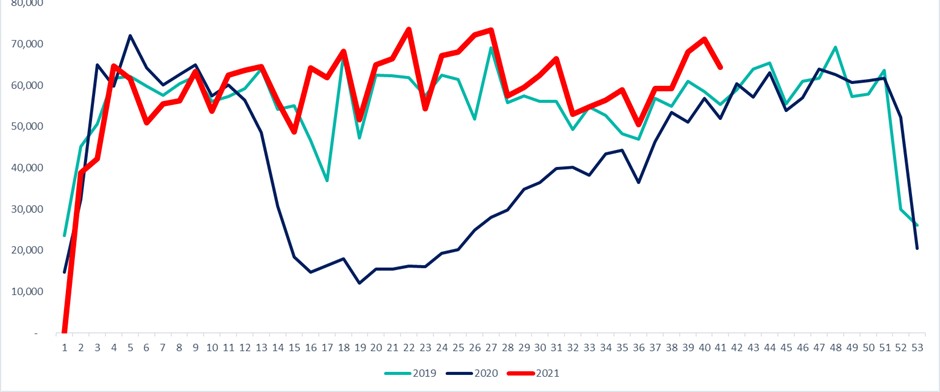

Billing volumes for insured hospital treatments have consistently out-performed pre-pandemic levels this year according to Healthcode which processes private medical invoices for the sector.

Speaking at Laing Buisson’s Private Acute Healthcare Conference in London on 14 October, Healthcode’s Managing Director, Peter Connor gave an overview of PMI billing trends in 2021. He revealed that hospital PMI volumes have superseded 2020 levels by 52% over the year to date and were up 6% on 2019.

Before the pandemic struck in early 2020, Healthcode processed around 27,000 medical bills every day on behalf of UK private hospitals and practitioners carrying out a series of checks and validations before passing it to one of the major Private Medical Insurers (PMIs) for payment. This billing data meant Healthcode had a unique benchmark to measure the impact of this turbulent period on the private healthcare sector and it has shared these year-on-year PMI billing trends over the last 18 months to guide and inform industry stakeholders.

As the graph shows, the story of 2021 has been largely positive for private hospitals, particularly from the start of Q2. Over the summer, billing volumes even exceeded those in 2019 by a significant margin: in June, for example, they were around 30% higher and in September they were running at 114% of 2019 levels. The trend suggests that private hospitals – like their NHS equivalents – are dealing with suppressed demand, as well as non-urgent treatments that had to be postponed because of the pandemic.

Regional variations

Of course, it has not been a uniform rate of recovery across the sector and from the beginning of the year there have been clear regional differences. In England, the volume of PMI bills rebounded from 89% of the pre-pandemic level in January to 114% in September, an average of 106% for the year to date. However, the year-on-year trend in London fell behind the rest of the country with billing volumes dipping below 2019 levels in several months, averaging 104% for the year to date. After this slow start, billing activity in the capital started to pick up pace again in late summer, reaching 115% of 2019 volumes in September.

In the rest of the UK, Northern Ireland has performed most strongly, averaging 104% of the 2019 billing volumes in the year to date. Meanwhile, Scotland has been averaging 101%, while Wales has lagged behind the other home nations with 99%.

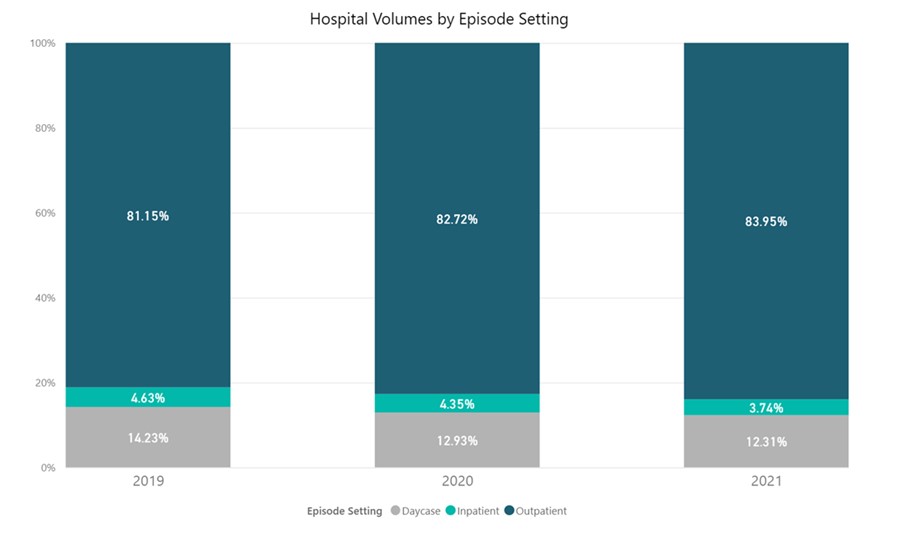

Variations by episode setting

The recovery in hospital billing volumes has been most striking for episodes of outpatient care but inpatient activity has lagged behind in 2021, even in the best performing hospital groups. In fact, billing for admitted patients was only 94% of pre-pandemic levels in September, compared with 119% for outpatients. The number of unique insured outpatients in September 2021 was 15% higher than 2019 while the number of unique insured admitted patients was 9% below the 2019 equivalent.

As the chart shows, the proportion of outpatient care has increased since the pandemic began. Outpatient care now makes up nearly 84% of billing volumes, compared with just over 81% in 2019. Meanwhile, inpatient episodes accounted for 14% of billing in 2019 but only 12% in 2021. However, it is too early to say if this trend will continue.

Variations by specialty

Orthopaedics continues to account for the bulk of private hospital activity despite the detrimental impact of the pandemic on the specialty. It was again the top hospital specialty in September 2021 with insured billing volumes of 49,000, double that of the next medical specialty (radiology). After slumping to just 12% of 2019 billing volumes during the first lockdown, billing volumes in September 2021 were 107% and are now consistently above 2019 levels.

Radiology and pathology/haematology are the medical specialties that have fared best over the course of the pandemic, reflecting demand for diagnostic tests and other investigations. In September 2021, hospital billing volumes compared with 2019 were 146% and 170% respectively. Other medical specialities have been consistently above pre-pandemic billing volumes in the second half of 2021 although the rate of recovery has been slower in ENT and urology.

Conclusion

Overall private hospital billing volumes have largely recovered in recent months but we cannot be sure this is a long-term trend, amid concerns over the rising infection rate and the possibility of further restrictions. Whatever twists the pandemic has in store, however, Healthcode’s billing data will continue to highlight the impact on private hospitals and provide a reliable measure of the sector’s resilience.